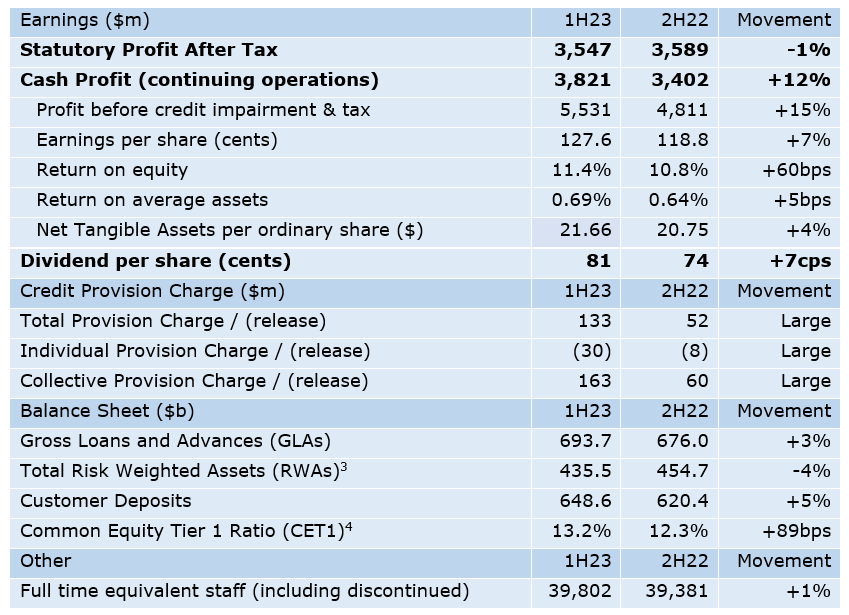

[1] today announced a Cash Profit[2] from continuing operations of $3,821 million, up 12% when compared with the prior half.

Statutory Profit after tax for the half year ended 31 March 2023 was $3,547 million.

ANZ’s Common Equity Tier 1 Ratio increased to 13.2% and Cash Return on Equity rose to 11.4%. The proposed Interim Dividend is 81 cents per share, fully franked.

GROUP FINANCIAL INFORMATION

ANZ Chief Executive Officer, Shayne Elliott, said: “This was a strong financial performance in which all four divisions made a material contribution. The record result was driven by solid revenue growth across the board and the benefits of having a well-diversified business. It was also a direct outcome of our deliberate strategy to simplify, reshape and de-risk the bank, which has allowed us to replace revenue following the disposal of non-core assets.

“Achievements this half included establishing a new Non-Operating Holding Company, completing the single largest regulatory program in our history (BS11), making further progress with our application to acquire Suncorp Bank, migrating our entire HR platform to the cloud and taking further steps to strengthen our ecosystem strategy, including by growing Cashrewards and investing in View Media Group.

“Australia Retail grew home loans faster than the market, while also driving good growth in deposits. We continued the rollout of ANZ Plus, which had $6 billion of deposits at end-April from over 250,000 customers, 30% of which were new to bank, with 39% new to bank in March.

“Institutional posted a record half-year result, producing returns well above the cost of capital in each region and strong revenue growth across all products. The division saw ongoing rapid growth in payments and currency processing and benefitted from servicing other financial institutions where we have a competitive advantage and significant market leadership. The international business performed strongly, contributing to more than 60% of the Division’s revenue growth compared with the prior comparable period.

“In New Zealand, revenue and returns were both up strongly compared with the first half of 2022 and we continue to lead the market in all of our target segments. The BS11 regulatory program, the single largest project in the Group’s history, is now complete. We are well positioned to continue growing the business while also supporting customers through an uncertain environment.

“Australia Commercial was a strong contributor to Group revenue, generating the highest return on equity of our divisions and delivering revenue growth of 30%[1] compared with the prior comparable period. During the half we performed particularly well supporting customers in agriculture, trade and manufacturing.

“We continued to tightly manage costs at a time of significant inflation and from a balance sheet perspective remain one of the best capitalised banks in the world. We were among the first banks in the world to successfully access global funding markets after a period of market instability, demonstrating the strength of our franchise and confidence in the Australian banking system. We have a well-diversified portfolio and the ability to allocate capital dynamically to maximise shareholder returns.”

DIVISIONAL HIGHLIGHTS

Australia Retail

- Revenue up 4% vs 2H22 or 11% vs 1H22, driven by restored home lending momentum from the previous half and deposit margin management in a highly competitive environment.

- Strong home loan momentum in the first half, supported by restored capability and capacity and an improved broker support model.

- Increased customer engagement in ANZ Plus, with deposits reaching $5.3 billion in 1H23 ($6 billion by the end of April). The average balance per customer increased 51% vs 2H22 and the onboarding process achieved a net promoter score (NPS) of +52.

Australia Commercial

- Revenue up 13% vs 2H22 or 11% vs 1H22, driven by disciplined margin management and a strong deposit franchise.

- Net Loans and Advances expanded by 4% vs 1H22 by maintaining strong momentum in priority sectors.

- Finalised the sale of the investment lending business in April 2023 and continued to build on strategic partnerships, including ANZ Worldline platform which is now live.

Institutional

- Revenue up 23% vs 2H22 or 35% vs 1H22 as the division continued to focus on payments processing and servicing of other financial institutions.

- Rapid growth in payments processing, with New Payments Platform agency payments increasing 31% vs 1H22 while platform cash management accounts grew 32% vs 1H22.

- Participated in 56 sustainable finance deals worth $75 billion, broadly comparable to prior half against the backdrop of volatile macroeconomic conditions.

- Revenue up 1% vs 2H22 or 14% vs 1H22, with margin expansion against a challenging competitive backdrop.

- Net Loans and Advances grew 3% vs 1H22 driven by home and business lending, despite a more challenging economic environment.

- Supported customers impacted by the floods and cyclone with emergency access to over $11 million of interest-free funds, as well as waiving ~$1.3 million in fees across February and March for our business and personal customers.

CREDIT QUALITY

The total credit impairment charge for the first half was $133 million, comprising:

- a collectively assessed provision (CP) charge of $163 million.

- an individually assessed provision (IP) release of $30 million.

The additional CP charge takes our total CP balance at 31 March 2023 to $4,040 million. Individual provisions remain at low levels, with writebacks and recoveries more than offsetting new provisions in the half.

ANZ Banking Group’s Common Equity Tier 1 Ratio is 13.2%, an increase of 89bps since September 2022. This increase included the impacts of APRA’s capital reforms, the majority of which were effective from January 2023. On a pro-forma basis, inclusive of the proposed Suncorp Bank acquisition and adjusted for the surplus capital in the Non-Operating Holding Company, the Banking Group’s capital ratio is 12.1%. This is above APRA’s revised expectations for major banks of between 11.0% and 11.5%.

The Board considers an Interim Dividend of 81 cents per share is appropriate for the current operating conditions. ANZ also stated the Dividend Reinvestment Plan will continue to apply for the Interim 2023 Dividend at no discount and the impact will be neutralised via the purchase of shares on market.

OUTLOOK

Mr Elliott said: “The next six months will be more difficult than the last. Competition in retail banking is as intense as it has ever been, both in Australia and New Zealand. We understand that sustained higher inflation and interest rates create further challenges for some households and businesses across the economy. While the number of ANZ customers in difficulty remains low, we stand ready to help in these potentially challenging times.

“We enter the next half with a business structure that brings the benefits of geographic and product diversification. We have a robust capital position, credit loss provisions higher than any other time pre-COVID, a strong and diverse deposit base and a track-record of execution. We are seeing continued momentum and high employee engagement across all four divisions, each with a clear strategy and a funded roadmap for growth.

“As the world is changing rapidly, ANZ is well placed to deploy our people and capital to help those facing challenges, but also support those looking for opportunities.”

Interviews with relevant executives, including Shayne Elliott, can be found at .

Approved for distribution by ANZ’s Continuous Disclosure Committee

[1] Following the establishment of the Non-Operating Holding Company in January 2023 ANZ Group Holdings limited replaced ANZ Banking Group Limited as the listed entity for the ANZ Group. The results represent the continuation of the ANZ Group.

[2] Cash Profit excludes non-core items included in Statutory Profit with the net after tax adjustment an increase from Statutory Profit of $274m.

[3] March 2023 RWA based on APRA revisions to capital adequacy requirements (APRA Capital Reform) effective 1 January 2023.

[4] ANZ Banking Group Level 2

[5] Adjusted for the net gain on sale from divested businesses recognised in the Australia Commercial division in the March 2022 half.